Best Home Loan Banks India 2026 — Rates Compared

Home Loan Best Home Loan Banks in India 2026 — Lowest Interest Rates Compared By CalcBharat.com Finance Team · April 2026 · 10 min read

Taking a home loan is probably the biggest financial decision of your life. A difference of just 0.5% in interest rate on a ₹50 lakh loan can mean ₹5–7 lakh difference in total interest paid over 20 years. Choosing the right lender matters enormously.

Here’s a comprehensive comparison of home loan rates from all major banks in India as of April 2026.

📌 🔢 Calculate your EMI instantly: Use our Free Home Loan EMI Calculator with any of the rates below.

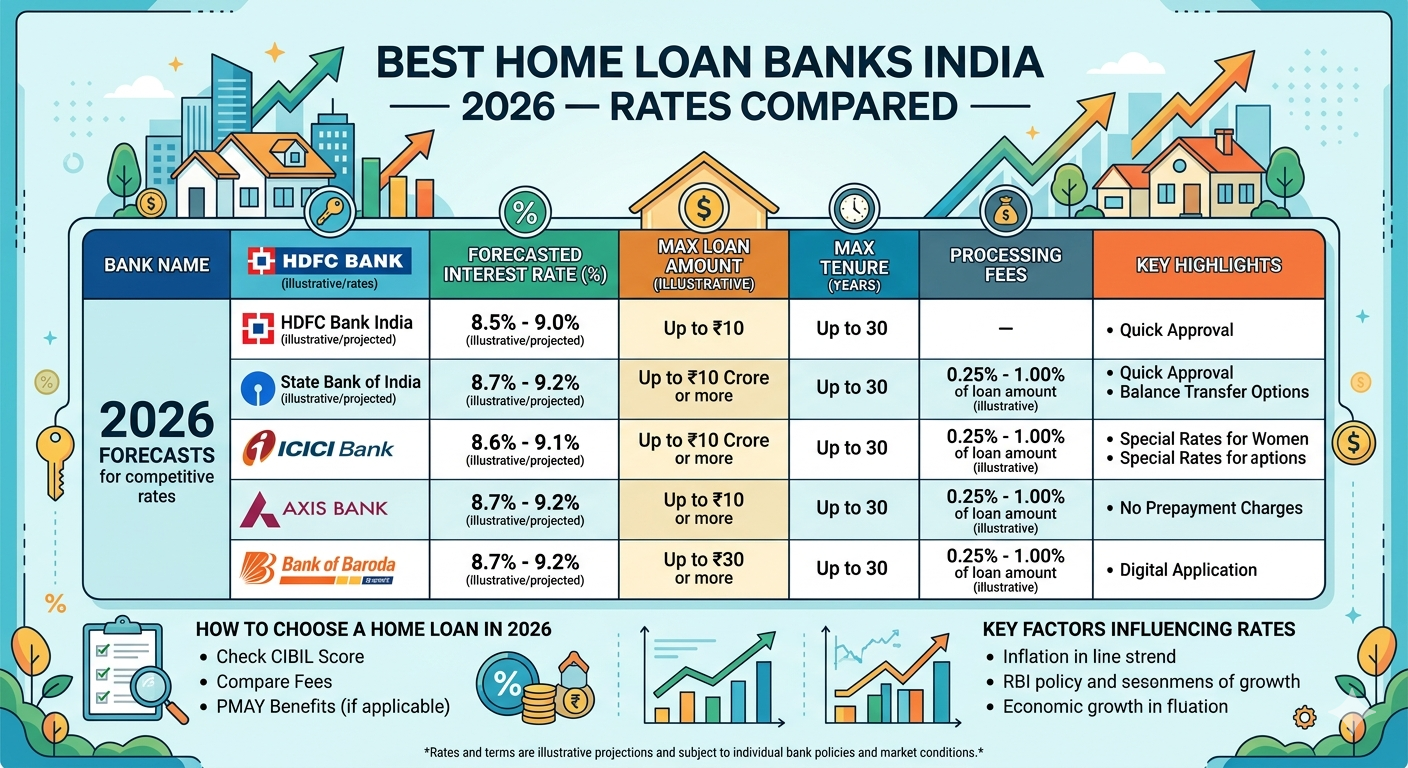

Home Loan Interest Rates — All Major Banks (April 2026)

| Lender | Starting Rate | Best Rate (CIBIL 750+) | Processing Fee | Best For |

SBI8.50%8.50%0.35% (max ₹10,000)Government employees, lower income |

HDFC Bank8.70%8.70%0.5% + GSTSelf-employed, faster approval |

ICICI Bank8.75%8.75%0.5–2% + GSTDigital-first, pre-approved offers |

Axis Bank8.75%8.75%1% + GSTFlexi EMI options, top-up loans |

Kotak Mahindra Bank8.75%8.70%0.5% + GSTHigh CIBIL score borrowers |

Bank of Baroda8.40%8.40%0.25–0.5%Lowest rate among PSU banks |

PNB Housing Finance8.50%8.50%Up to 0.50%Flexible eligibility, tier-2 cities |

LIC Housing Finance8.50%8.50%₹10,000–₹15,000Salaried employees, LIC policyholders |

Bajaj Housing Finance8.55%8.55%Up to 4%High loan amount, quick processing |

Tata Capital8.75%8.75%Up to 2%Self-employed, NRIs |

*Rates as of April 2026. All rates are floating, linked to repo rate. Actual rate depends on your CIBIL score, income, loan amount, and LTV ratio. Always verify with the lender.

EMI Comparison — ₹30 Lakh Loan, 20 Years

| Rate | Monthly EMI | Total Interest (20 yrs) | Total Payment |

8.40% (Bank of Baroda)₹25,832₹31.99 lakh₹61.99 lakh |

8.50% (SBI)₹26,035₹32.48 lakh₹62.48 lakh |

8.75% (HDFC/ICICI)₹26,530₹33.67 lakh₹63.67 lakh |

9.00%₹26,992₹34.78 lakh₹64.78 lakh |

9.50%₹27,992₹37.18 lakh₹67.18 lakh |

The difference between 8.40% and 9.50% on a ₹30 lakh loan over 20 years: ₹5.19 lakh in extra interest. That’s why shopping for the best rate matters.

What Determines Your Home Loan Interest Rate?

- CIBIL Score: The biggest factor. Score above 800 = lowest rates. Below 700 = significantly higher rates or rejection. Check your score free at CIBIL.com once a year.

- Loan-to-Value (LTV) Ratio: Lower LTV = lower risk for bank = lower rate. If you pay 30% down payment instead of 20%, you’ll often get a better rate.

- Income Stability: Government employees and large company salaried employees get better rates. Self-employed borrowers often pay 0.25–0.5% more.

- Loan Amount: Larger loan amounts often attract marginally lower rates as the fixed processing cost is spread over a larger base.

- Property Type: Ready-to-move-in properties often get slightly better rates than under-construction, due to lower risk for the bank.

How to Get the Lowest Home Loan Rate — 5 Practical Steps

- Get your CIBIL score above 750 before applying (pay all EMIs/credit cards on time for 6+ months)

- Get pre-approval letters from 3–4 banks before choosing — use competing offers to negotiate

- Use a DSA (Direct Selling Agent) or loan aggregator like Paisabazaar — they negotiate rates on your behalf

- Opt for a shorter tenure if you can afford higher EMI — you pay much less total interest

- Make a higher down payment if possible — reduces LTV and often unlocks better rate

SBI vs HDFC Home Loan — Which is Better?

| Factor | SBI Home Loan | HDFC Bank Home Loan |

Interest Rate8.50% (lowest PSU)8.70% (competitive) |

Processing SpeedSlower (7–15 days)Faster (3–7 days) |

Processing FeeLower (0.35%)Higher (0.5%+) |

Prepayment PenaltyNone (floating rate)None (floating rate) |

Top-up LoanAvailableAvailable |

Best ForCost-conscious, government employeesSpeed, self-employed, NRIs |

For most salaried employees who prioritise lowest cost: SBI wins on rate. For self-employed and those needing faster processing: HDFC/ICICI are better.

📌 📖 Also read: 7 Smart Ways to Reduce Your Home Loan EMI in 2026 →

📌 🏠 Plan your loan: EMI Calculator — Instant Home Loan EMI Calculation →

🏠

CalcBharat.com Finance Team Home Loan & Mortgage Experts Interest rates sourced from bank websites and verified as of April 2026. Home loan rates change with RBI repo rate decisions. Always verify current rates with the lender before applying. This is not financial advice.

Frequently Asked Questions

Ready to calculate? Get instant accurate results.

Calculate Your Home Loan EMIFrequently Asked Questions

SBI currently starts at 8.50% p.a. for salaried borrowers with a 750+ CIBIL score. HDFC, LIC HFL and Bank of Baroda are close. Your exact rate depends on your credit score, income stability, and loan amount.

750 or above. Below 700, you typically get a 0.25–0.50% rate penalty or rejection. A 750+ score on a ₹30 lakh loan at 20 years can save you ₹3–5 lakh in total interest compared to a 680 score.

For lowest rates and government/PSU employees — SBI. For faster processing and self-employed borrowers — HDFC. The rate difference is usually 0.10–0.25%. Check both with your actual profile before applying.

Yes, this is a balance transfer. If your current rate is 0.50%+ above market, it’s worth calculating the savings. Switching has a processing fee (0.5–1% of outstanding). It’s most beneficial in the first 5–7 years when interest component is highest.

Typically 0.25%–1% of the loan amount, capped at ₹10,000–₹30,000. SBI charges a flat fee. HDFC charges up to 0.5%. Always negotiate — banks frequently waive or halve this fee for good-profile applicants.