7 Smart Ways to Reduce Your Home Loan EMI in 2026

Home Loan 7 Smart Ways to Reduce Your Home Loan EMI in India (2026) By CalcBharat.com Finance Team · April 2026 · 8 min read

If you took a home loan in the last 2–3 years when interest rates were high, you might be paying a significantly higher EMI than you need to. With RBI cutting repo rates and multiple lenders offering competitive rates in 2026, there are real opportunities to reduce your monthly burden.

In this guide, we’ll walk you through 7 proven strategies that can help you reduce your home loan EMI — backed by real numbers and examples.

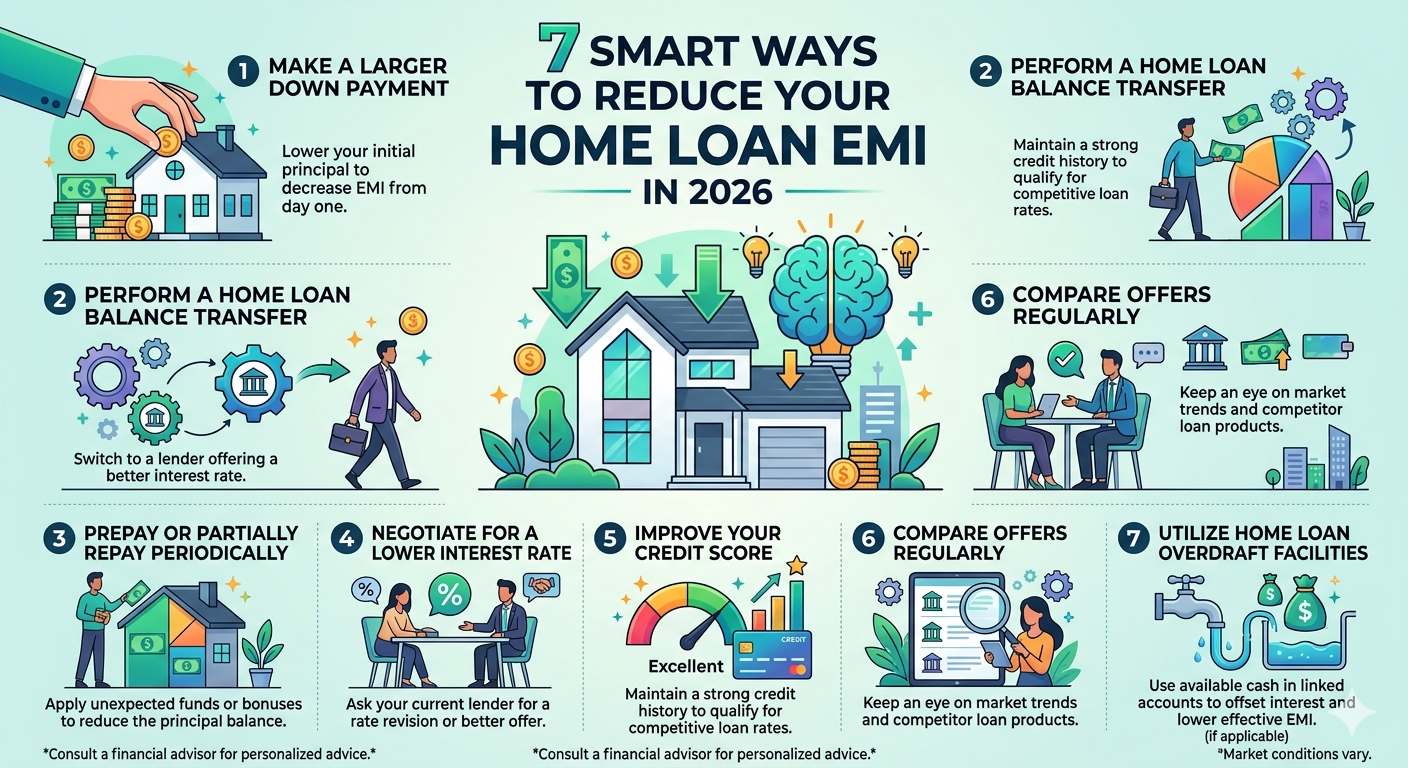

1. Make Part Prepayments (Most Effective)

Prepaying even a small lump sum — say ₹1–2 lakh per year — can dramatically reduce your total interest burden. When you make a prepayment, the entire amount goes toward reducing your principal. This reduces the base on which interest is calculated for all future months.

Example: ₹30 lakh home loan at 8.5% for 20 years. Regular EMI = ₹26,035. If you prepay ₹2 lakh in Year 1, you save approximately ₹4.8 lakh in total interest and can close the loan 2 years earlier.

📌 💡 Tip: For floating rate home loans, RBI mandates that banks cannot charge any prepayment penalty. So you can prepay any amount, any time, for free.

2. Do a Home Loan Balance Transfer

If your current lender is charging 9.5% and another bank is offering 8.75%, a balance transfer can save you significant money. Even a 0.5% rate reduction on a ₹50 lakh loan can save over ₹5 lakh in interest over the remaining tenure.

How it works: Your new lender pays off your existing loan and you start a fresh loan at the lower rate. Processing fees apply (typically 0.5–1% of outstanding loan), so calculate break-even before transferring.

3. Increase Your Loan Tenure

If you need immediate cash flow relief, you can request your bank to increase the tenure of your loan. This directly reduces your monthly EMI.

Example: ₹40 lakh loan at 8.5% — 15-year tenure: EMI ₹39,376. 20-year tenure: EMI ₹34,720. Extending by 5 years reduces EMI by ₹4,656/month — though total interest paid increases.

4. Negotiate a Lower Interest Rate with Your Bank

If your CIBIL score has improved since you took the loan, or if your bank is offering new customers a lower rate, you have grounds to negotiate. Many banks allow existing customers to switch to a lower rate by paying a nominal conversion fee (₹5,000–₹10,000).

Write a formal request to your bank’s branch manager, citing: your excellent repayment track record, current market rates, and competing offers you’ve received.

5. Improve Your CIBIL Score Before Applying

If you’re planning to take a new home loan, your CIBIL score is the single biggest factor determining your interest rate. Borrowers with scores above 800 typically get rates 0.5–1% lower than those with scores of 700–750.

- Pay all credit card bills and EMIs on time

- Keep credit utilization below 30%

- Don’t apply for multiple loans simultaneously

- Check your credit report annually for errors

6. Opt for a Floating Rate Loan

In a falling interest rate environment (like 2024–2026 with RBI rate cuts), a floating rate loan benefits you automatically. Your EMI decreases as the RBI repo rate falls. Fixed rate loans don’t benefit from rate cuts but protect you during rate hike cycles.

7. Use Your Annual Bonus / Increments for Prepayment

A disciplined approach: every year, use your Diwali bonus or salary increment to make a lump sum prepayment. Even ₹50,000–₹1 lakh per year consistently applied to principal can cut your loan tenure by 4–5 years.

📌

📊 Try our Free EMI Calculator to see exactly how much you can save with different prepayment amounts and rate reductions.

Summary: Which Strategy is Best?

| Strategy | Effort | Savings Potential | Best For |

Part PrepaymentLowVery HighAnyone with savings |

Balance TransferMediumHighHigh loan outstanding |

Extend TenureLowEMI ReliefCash flow stress |

Rate NegotiationLowMediumGood CIBIL score |

Improve CIBILMediumHigh (new loans)Planning new loan |

👨💼

CalcBharat.com Finance Team Personal Finance & Banking Experts This article has been reviewed by our finance team for accuracy. All examples use indicative rates and actual results may vary. Please consult a financial advisor before making major loan decisions.

Frequently Asked Questions

Ready to calculate? Get instant accurate results.

Calculate Your New EMIFrequently Asked Questions

Part prepayment — even ₹1–2 lakh in the first 5 years eliminates multiple future EMIs and saves lakhs in interest due to compounding. Most floating rate home loans have zero prepayment penalty (RBI mandate). Use any bonus or windfall for this.

Yes. Three ways: (1) negotiate with your bank directly, (2) transfer balance to a lower-rate lender, (3) switch from MCLR to RLLR (repo-linked rate) if your bank still offers MCLR. Each can save ₹500–₹2,000/month on a ₹30L loan.

On a ₹30L loan at 8.5%: extending from 15 to 20 years cuts EMI by ₹3,491/month (₹29,526 → ₹26,035). But you pay ₹15–20L more total interest. Use only if cash flow is genuinely tight — don’t extend tenure just for comfort.

Moving your outstanding loan to a bank offering a lower rate. On ₹30L outstanding, a 0.50% reduction saves ~₹8,000–10,000/year. Processing fee (₹10K–20K) is typically recovered within 12–18 months. Most beneficial in the first half of the loan tenure.

It doesn’t reduce EMI directly, but increases eligible loan amount and may get a 0.05–0.10% rate concession (some banks offer this for women co-borrowers). Most useful when the primary applicant’s income alone doesn’t qualify for the needed loan amount.